Navigating Medicare Enrollment and Coverage Strategies

🤔 Medicare Doesn’t Have to Be Confusing

When you’re approaching 65, conversations about Medicare start to pop up everywhere—mailers, emails, HR updates, and well-meaning advice from colleagues, friends and family.

But here’s the thing: Medicare is not a one-size-fits-all system. The choices you make—when to enroll, which plan to pick, how to cover prescriptions—can impact your healthcare costs for decades.

In our recent Medicare Education Webinar, we covered the essentials: Parts A and B, enrollment timing, supplemental coverage (Medigap), Advantage Plans, and drug coverage. We also dug into strategies for people working past 65 as well as those dreaming of retiring early.

Here’s the breakdown so you can feel confident instead of overwhelmed.

Medicare Parts A and B: The Basics

Part A (Hospital Coverage):

Covers inpatient hospital care, skilled nursing, hospice, and some home health services. Premium-free for most people who paid Medicare taxes while working.Part B (Outpatient Coverage):

Covers doctor visits, outpatient care, preventive services, and durable medical equipment.Premium in 2025: $185/month (higher for incomes above $106,000 single / $212,000 married).

Annual deductible: $257, after which Medicare pays 80%.

If you’re already collecting Social Security, you’ll be automatically enrolled at 65- and your Medicare premiums will be deducted directly from your Social Security checks. Otherwise, you’ll need to sign up – and work with the Social Security Administration to coordinate paying your premiums.

And pay attention!! Missing the right window can mean late-enrollment penalties.

🏃♀️ Working Past 65: Do You Need Medicare Right Away?

Here’s where a lot of people get tripped up. If you’re still working at 65 and have employer coverage:

If your employer has 20+ employees: You can delay Part B without penalty as long as your employer coverage is considered “creditable.”

If your employer has fewer than 20 employees: You should enroll in Medicare Part A and B at 65 to avoid gaps and penalties.

💪🏽 Pro tip: Contact Social Security about two to three months before retiring to time your Part B coverage to start when your employer plan ends.

Supplemental Coverage:

Medigap in Massachusetts

Original Medicare (Parts A + B) doesn’t cover everything. That’s where Medigap comes in.

In Massachusetts, there are three standardized Medigap plans:

Core Plan: Lower premium (~$120/month) but leaves you on the hook for the Part A deductible ($1,676 in 2025).

1A Plan: Mid-range coverage (~$150–$200/month).

Plan 1: More comprehensive, covering hospital deductibles and coinsurance (~$200–$260/month) – however, note, that this is mostly no longer available to most workers.

Medigap plans are great if you want predictability and flexibility—no networks, and you can see any doctor who accepts Medicare nationwide.

💊 Prescription Coverage: Medicare Part D

If you go with Original Medicare + Medigap, you’ll need to add a Part D prescription drug plan.

Premiums range from $8 to $100+ per month depending on coverage.

Optional deductible (up to $590).

In 2025, once you spend $2,000 out of pocket, the plan covers 100% of your prescriptions.

When choosing a Part D plan, don’t just look at premiums—make sure your actual prescriptions are covered affordably. Tools like Medicare.gov or the professionals at the Mass College of Pharmacy can help you understand and compare drug costs.

✅ Medicare Advantage Plans: All-in-One Option

Medicare Advantage (Part C) plans bundle Parts A, B, and often D.

Many plans have low or $0 premiums but require copays for services.

Plans may include extras like dental, vision, hearing, gym memberships.

Plans have an annual out-of-pocket maximum (something Original Medicare + Medigap doesn’t).

Plans are typically HMO or PPO networks—meaning less flexibility compared to Medigap.

Important: Advantage Plans should be re-evaluated each year during the Annual Election Period (Oct 15–Dec 7) because coverage and drug formularies change.

✈️ Travel Considerations

💪🏽 Pro tip: Do you dream of travelling in retirement?

Original Medicare provides limited coverage outside the U.S.

Some Medigap and many Advantage Plans include worldwide emergency coverage.

Supplemental travel health insurance, such as GeoBlue, can fill the gap if you’re a frequent traveler.

🌉 Retiring Before 65: Bridging the Gap

If you’re not yet Medicare-eligible but would love to leave your job, it’s all about comparing costs and coverage until Medicare kicks in. Here are your options:

Spousal coverage: if your spouse is still working, get onto his health plan, as retirement is considered a qualifying event.

COBRA: This allows you to extend employer coverage 18–36 months. Note, this is often expensive.

Direct-purchase plans: another option is to purchase a private health insurance plan through the Health Insurance Marketplace or MassHealth Connector. If you’re a business owner, this expense is often deductible.

Real-World Questions from our recent Medicare Webinar:

Participant A: I’m planning on retiring soon – when do I need to contact Medicare? You should reach out to Medicare two to three months before your retirement date to start Part B.

Participant B: I have several prescriptions I take regularly, what should I do? Start looking at Part D Drug plan options by plugging in your medications.

Participant C: I’m also dreaming of retiring early, what are my options? You should be weighing COBRA vs. spousal coverage vs. marketplace plan.

These examples highlight how personal Medicare choices really are. Your situation—retirement date, prescriptions, travel habits, and employer coverage—all matter.

FAQs About Medicare Enrollment:

1. What happens if I delay signing up for Medicare Part B?

If you don’t have “creditable” coverage from an employer (20+ employees) and you delay enrolling, you could face lifetime penalties added to your monthly premium. Always double-check with your employer’s HR before making a decision.

2. Do I need both Medigap and Part D?

Yes, if you’re choosing Original Medicare. Medigap covers gaps in Parts A and B (like coinsurance and deductibles), while Part D covers prescriptions. They work together.

3. Can I switch from Medicare Advantage to Medigap later?

You can, but it’s not always guaranteed. In Massachusetts, there’s more flexibility because of continuous Medigap open enrollment. In other states, medical underwriting may apply. Check your state’s rules before switching.

4. Will my Medicare premiums change often?

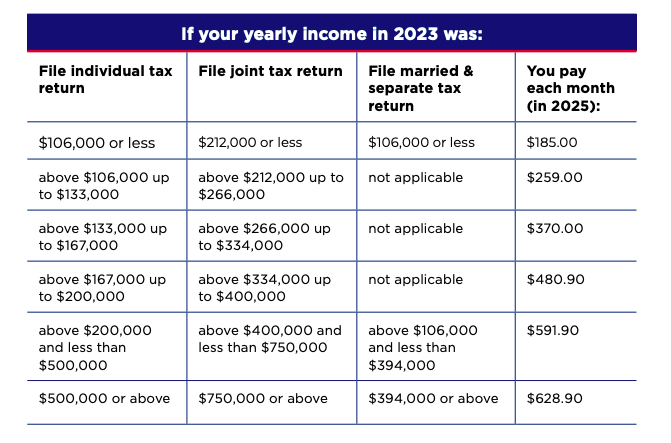

Yes! It is so important to understand your own financial plan, as your income dictates how much you’ll pay for Part B premiums. In 2025, you can see the chart showing the additional surcharges at various income levels. Very few people realize that by working with your wealth and tax management team, we can help you avoid unnecessary Medicare surcharges via proactive management of your income and capital gains exposure.

5. What is the Medicare donut hole?

Prior to January 2025, the donut hole was a temporary limit on what the drug plan would cover for drugs. Now all Medicare plans include a $2,000 cap on what you pay out-of-pocket for prescription drugs covered by your plan.

Key Medicare Dates to Remember:

Initial Enrollment Period: Around your 65th birthday (3 months before, month of, 3 months after).

Annual Election Period (AEP): Oct 15–Dec 7. Switch Advantage Plans or Part D.

Special Enrollment Periods: For those retiring after 65 with employer coverage.

The Bottom Line:

Medicare is one of the most important parts of your retirement plan—but also one of the most confusing. The good news? With the right information and guidance, you can make choices that protect your health and your wallet.

Whether you’re retiring at 65, still working, or traveling the world, the key is to plan ahead:

Review your employer benefits.

Compare Medigap vs. Advantage.

Look at your prescription drug coverage.

Put key enrollment dates on your calendar.

And remember—you don’t have to figure it out alone.

👉 Need help figuring out your Medicare strategy?

As both a financial planner and an Enrolled Agent, I help clients integrate healthcare planning with their retirement and tax strategies. Schedule a call with me today.

🐝 FAQ: Smart Medicare Enrollment & Coverage Strategies for High Earners

When should I enroll in Medicare if I’m still working or have employer coverage?

If you’re still working past age 65 and your employer plan meets “creditable coverage” standards, you may be able to delay enrollment in Parts A or B without penalty. But you must verify how that interacts with your employer-plan, when you retire or change coverage, and the deadlines for switching. {cite}turn0search2{cite}{cite}turn0search0{cite}

How do I choose between Original Medicare + Medigap vs Medicare Advantage (Part C) for my wealth profile?

Original Medicare offers broad provider access, but you’ll likely need a Medigap plan to minimize out-of-pocket risk. Medicare Advantage bundles coverage, often with extra benefits, but network restrictions and benefit changes merit careful review—especially for higher-income individuals with complex needs or travel. {cite}turn0search5{cite}{cite}turn0search1{cite}

What enrollment periods and deadlines should I never miss?

Key periods: Initial Enrollment Period (IEP) = 3 months before your 65th birthday through 3 months after. Annual Election Period (AEP) for plan changes = Oct 15-Dec 7. Medicare Advantage Open Enrollment = Jan 1-Mar 31 if you’re already in a MA plan. Missing the window may trigger lifelong penalties or limit your options. {cite}turn0search0{cite}{cite}turn0search1{cite}

How will my income affect my Medicare costs and strategy?

For high earners, Medicare premiums may be higher due to IRMAA (income-related monthly adjustment amount). Your modified AGI and tax strategy can impact Part B & D premiums, making tax planning (Roth conversions, HSA use, income timing) relevant to Medicare cost management. {cite}turn0news17{cite}

What should I check annually even if I’ve already enrolled?

Each year review your doctors and pharmacies (network), formulary for prescriptions, benefits & co-pays, and out-of-pocket maximums. Plans change each year—what worked one year may cost significantly more the next. {cite}turn0search1{cite}